IDC: India’s Smartphone Market Slows, but vivo Still Holds the Crown

India’s smartphone market entered 2026 on uncertain footing. After years of aggressive expansion fueled by affordable Android devices and festive-season sales, the country’s smartphone industry has now recorded a notable slowdown. According to new data from IDC, smartphone shipments in India fell 4.1 percent year-on-year during the first quarter of 2026, reaching 31 million units. Yet despite weaker shipment volumes, the market’s total value still rose by 5.8 percent, signaling a deeper structural transformation underway across the industry.

At the center of this transition is a dramatic shift in consumer behavior, rising smartphone prices, and an industry increasingly shaped by global AI infrastructure demand. While entry-level phones struggled badly, premium and mid-range devices continued to gain traction. Through it all, vivo retained its dominance as India’s top smartphone brand, even as competitors like OPPO and Motorola posted stronger growth rates.

India’s Smartphone Market Is Changing

For years, India has been regarded as one of the world’s most important smartphone battlegrounds because of its massive population and price-sensitive consumers. Brands traditionally relied heavily on affordable devices under $100 to drive massive shipment volumes. But IDC’s latest report suggests that model is becoming increasingly difficult to sustain.

The primary trigger behind the slowdown is the sharp increase in memory component prices. A global shortage of DRAM and NAND flash memory — fueled largely by the AI boom — has pushed smartphone manufacturing costs significantly higher.

As AI companies worldwide invest heavily in data centers and AI servers, memory manufacturers have shifted production toward high-bandwidth memory chips used in artificial intelligence infrastructure. That has reduced the availability of memory components for smartphones and other consumer electronics.

The impact has been particularly severe in India, where affordability remains one of the biggest purchasing factors.

IDC noted that many smartphone companies anticipated further price increases and aggressively stocked inventory ahead of time. However, consumer demand failed to keep pace, creating a mismatch between shipments and actual market absorption.

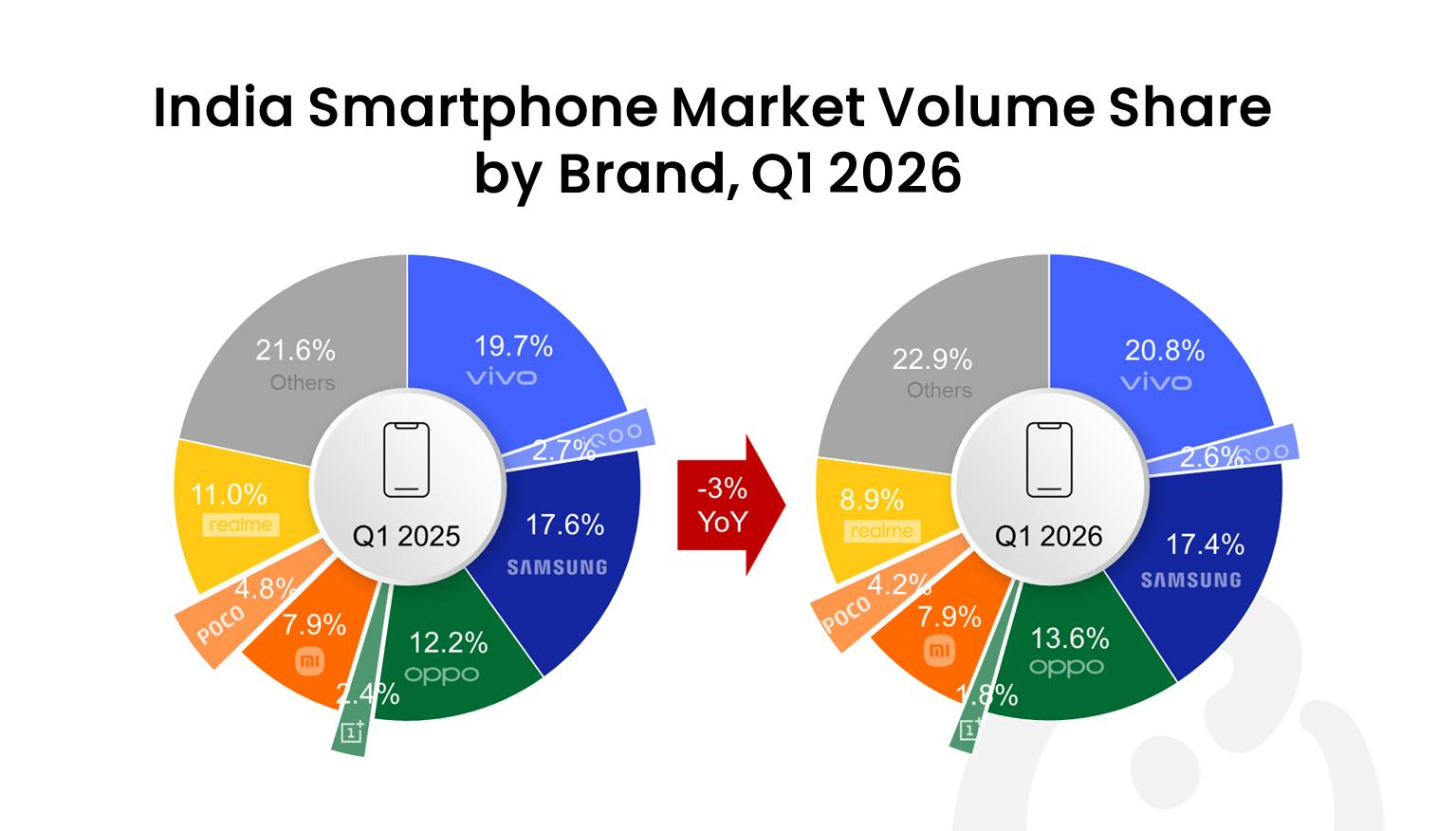

vivo Continues to Lead the Market

Despite the broader market slowdown, vivo maintained its position as India’s leading smartphone brand in Q1 2026.

The company secured a 19.6 percent market share during the quarter, only slightly lower than the 19.7 percent share it held a year earlier. Its shipments declined roughly in line with the broader market, allowing it to preserve its dominance.

Samsung remained in second place with a 17.1 percent market share and relatively flat shipment growth. The company benefited from its strong offline retail presence and broad portfolio spanning budget to premium smartphones.

OPPO emerged as one of the biggest winners of the quarter. The company recorded a remarkable 22 percent year-on-year growth, increasing its market share from 12 percent to 15.3 percent. IDC identified OPPO as the fastest-growing major smartphone brand during the quarter.

Apple also maintained strong momentum in India’s increasingly premium-focused market. While iPhone shipments dipped modestly, Apple still ranked fourth with a 9.4 percent market share. IDC highlighted that Apple continued to dominate the market in terms of value share, accounting for 28 percent of total smartphone market value in India.

Motorola was another standout performer. The brand grew shipments by 14 percent and expanded its market share to 8.9 percent, entering IDC’s top five rankings for the first time.

Budget Smartphone Brands Face Growing Pressure

While premium-focused brands showed resilience, several companies heavily dependent on online sales and budget devices struggled badly.

Realme experienced one of the sharpest declines among major brands, with shipments dropping 20 percent year-on-year. Poco saw a 14 percent decline, while iQOO suffered an even steeper 23 percent fall.

OnePlus endured the most severe decline among the top 10 smartphone brands. Its shipments fell by 32 percent compared to Q1 2025, causing its market share to shrink from 2.4 percent to just 1.7 percent.

Xiaomi managed to avoid major losses, recording modest 3 percent growth despite intense pressure in the affordable smartphone category. When combined with Poco, Xiaomi’s broader ecosystem still retained considerable influence in the Indian market.

Entry-Level Smartphones Are Collapsing

Perhaps the most important takeaway from IDC’s report is the rapid collapse of the ultra-budget smartphone segment.

Shipments of smartphones priced below $100 plunged by 59 percent year-on-year, with the category’s market share shrinking from 18 percent to just 8 percent.

IDC says consumers are now being “pushed upmarket by necessity rather than aspiration.”

In other words, buyers who previously purchased ultra-cheap smartphones are now being forced to spend more simply because manufacturers can no longer profitably produce devices at those low price points.

The strongest growth instead came from higher-priced categories:

- Premium smartphones priced between $600 and $800 grew 32 percent

- Mid-premium devices between $400 and $600 rose 29 percent

- The $100–200 segment expanded 10 percent

Meanwhile, India’s average smartphone selling price climbed to a record $302 during Q1 2026, up 10.4 percent year-on-year.

This represents one of the clearest signs yet that India’s smartphone market is evolving from a purely volume-driven industry into a value-driven one.

Offline Retail Is Winning Again

Another major trend emerging from IDC’s data is the resurgence of offline retail channels.

Physical stores now account for 62 percent of smartphone sales in India, up from 58 percent a year ago. Online sales, by contrast, declined from 42 percent to 38 percent of the market.

The shift reflects changing consumer priorities. Higher-priced smartphones are often purchased through offline stores where customers can receive demonstrations, financing options, exchange offers, and after-sales support.

IDC noted that rising prices also limited brands’ ability to run aggressive online discounts and flash sales, which had historically driven massive e-commerce growth in India’s smartphone sector.

The Global AI Boom Is Reshaping Smartphones

What makes this slowdown particularly significant is that it is not purely an India-specific issue.

Globally, smartphone shipments also declined during Q1 2026, falling 2.9 percent year-on-year to 293.8 million units after 10 straight quarters of growth.

The growing influence of AI infrastructure spending is now affecting the broader consumer electronics industry. As memory manufacturers prioritize AI servers and data-center hardware, smartphone makers are being forced to rethink pricing strategies, product portfolios, and profitability models.

IDC analyst Aditya Rampal explained:

“The current environment signals a broader structural shift in the market, where brands may increasingly need to rely on product differentiation, financing offers, and premiumization strategies rather than price-led promotions to drive demand through the remainder of 2026.”

What Happens Next?

IDC believes the first half of 2026 may remain relatively stable because smartphone companies still have access to previously purchased component inventories. However, many brands are reportedly lowering annual shipment targets and carefully managing inventory levels, especially in the entry-level segment.

The second half of the year could depend heavily on several factors:

- Whether global memory prices stabilize

- The strength of India’s festive-season sales

- Consumer confidence in a high-price environment

- The availability of financing and EMI programs

- Currency fluctuations and rupee depreciation

IDC Research Manager Upasana Joshi warned that prices may continue rising through 2027 if the memory shortage persists.

“Consumers considering an upgrade may find better value in purchasing sooner, as pricing pressures are expected to intensify over the coming quarters.”

A Turning Point for India’s Smartphone Industry

India’s smartphone market is no longer defined solely by cheap devices and explosive shipment growth. The latest IDC figures show an industry entering a new phase — one where profitability, premiumization, and value matter more than raw unit volumes.

vivo may still sit comfortably at the top of the rankings, but the broader competitive landscape is shifting quickly. OPPO and Motorola are gaining momentum, Apple continues strengthening its premium presence, and budget-focused brands face mounting pressure from rising costs and weaker consumer demand.

The biggest question now is whether India’s massive smartphone market can successfully adapt to an era where affordability is no longer guaranteed.