S&P 500 in Focus: Markets at a Crossroads in 2026

(Industry & Market Analysis)

- Introduction: Why the S&P 500 Still Matters

- A Benchmark Under Pressure: Recent Market Performance

- Structural Changes: Who Gets In—and Who Gets Out

- Sector Divergence: Winners and Strugglers

- Consumer Pressure and Market Sentiment

- Earnings Season: The Next Major Catalyst

- Technical Outlook: Key Levels and Market Signals

- The Bigger Picture: What the S&P 500 Represents Today

- Conclusion: A Market Defined by Tension—and Opportunity

Introduction: Why the S&P 500 Still Matters

The S&P 500—formally known as the S&P Dow Jones Indices flagship benchmark—remains the most closely watched gauge of the U.S. stock market and, by extension, global economic sentiment. Tracking 500 of the largest publicly traded companies in the United States, it serves as both a barometer of corporate performance and a foundation for trillions of dollars in investments.

In 2026, the index is navigating a complex landscape shaped by inflation pressures, geopolitical risks, sector rotation, and evolving corporate fundamentals. Recent developments—from index rebalancing decisions to diverging industry performance—underscore how dynamic and consequential the S&P 500 continues to be.

A Benchmark Under Pressure: Recent Market Performance

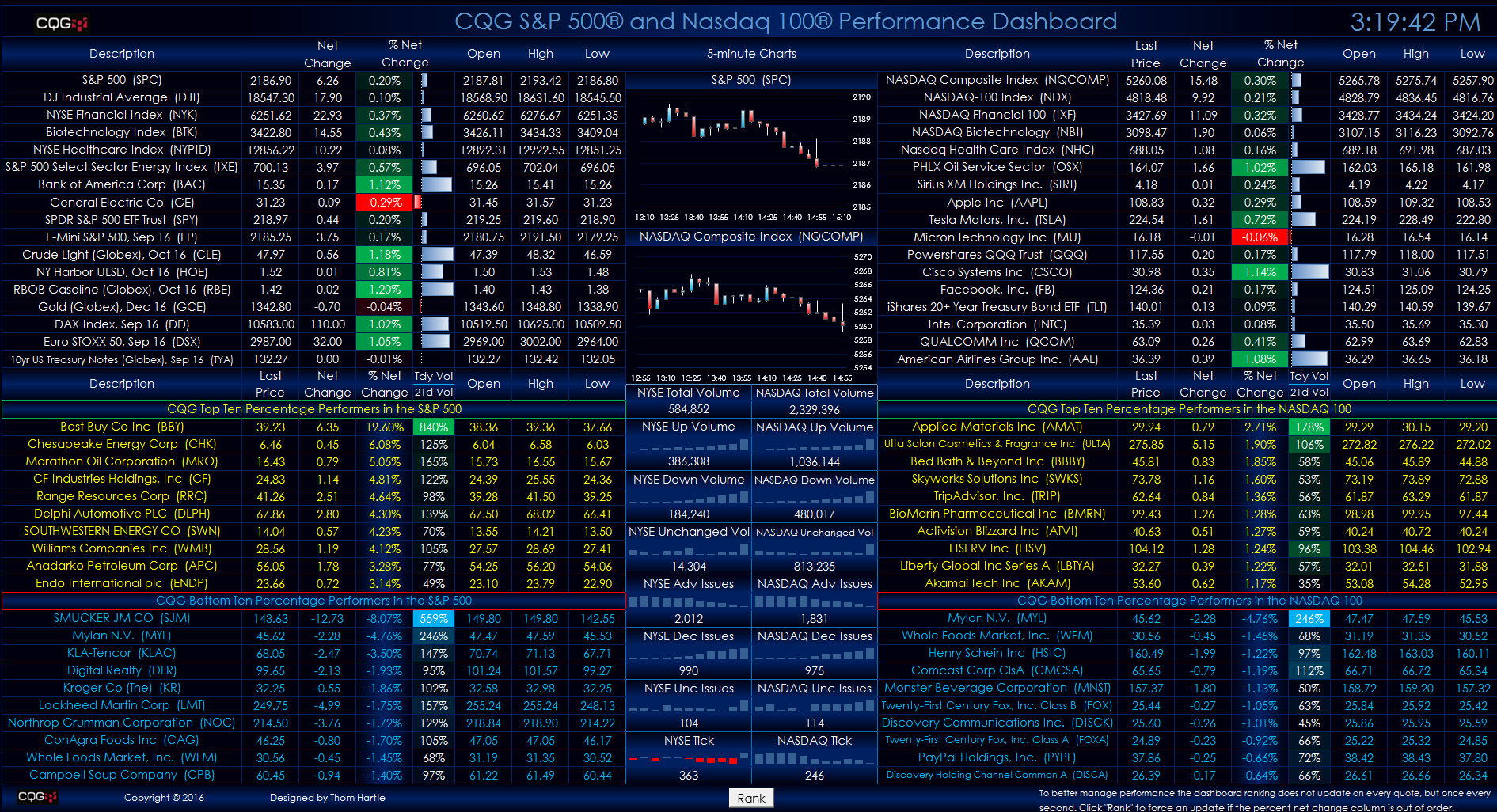

The S&P 500 has experienced notable volatility in early 2026. After reaching an all-time high above 7,000, the index retraced sharply before stabilizing near the 6,600 level, reflecting a fragile recovery.

Several macroeconomic forces are driving this behavior:

- Persistent inflation: Rising service-sector prices and elevated oil costs continue to pressure corporate margins.

- Interest rate uncertainty: Expectations that the Federal Reserve may delay rate cuts have weighed on valuations.

- Geopolitical tensions: Conflicts affecting global energy markets have pushed oil prices higher, impacting both consumers and businesses.

Despite these headwinds, the index recently posted a 3.4% weekly gain, signaling resilience even as underlying conditions remain unstable.

However, market breadth tells a more cautious story. Fewer than half of the index’s constituents are trading above long-term averages, suggesting that gains are concentrated in a limited number of stocks rather than broadly distributed.

Structural Changes: Who Gets In—and Who Gets Out

One of the defining features of the S&P 500 is its evolving composition. Companies are added or removed based on market capitalization, liquidity, and sector representation.

A recent development illustrates this process clearly:

- Casey’s General Stores is being added to the S&P 500.

- It replaces Hologic Inc., a healthcare firm exiting the index.

This change, announced by S&P Dow Jones Indices, takes effect before trading opens on Thursday.

Why This Matters

Index inclusion is not symbolic—it has real financial implications:

- Passive funds and ETFs tracking the S&P 500 must buy newly added stocks, increasing demand.

- Removed companies often face selling pressure, as index funds rebalance.

- Inclusion signals that a company has achieved a certain scale and stability in the market.

For Casey’s General Stores, the move reflects the growing relevance of consumer-focused retail businesses within the broader U.S. economy.

Sector Divergence: Winners and Strugglers

While the S&P 500 as a whole has faced modest declines—down approximately 2–3% over a recent six-month period—sector-level performance reveals a far more nuanced picture.

Technology and Semiconductors Surge

The semiconductor industry has delivered a 28.8% gain over six months, significantly outperforming the broader index.

This surge is driven by:

- Increasing demand for data processing and AI-related infrastructure

- Long-term growth in digital services and cloud computing

- Strategic importance of chips in global supply chains

Companies such as KLA Corporation are highlighted for their durable competitive positioning in this space.

Companies Facing Headwinds

Not all firms have benefited from these trends:

- Semtech Corp. has seen declining operating margins due to rising costs.

- Kulicke & Soffa Industries Inc. has struggled with falling sales and earnings.

These contrasts demonstrate a critical point: sector growth does not guarantee company-level success.

Consumer Pressure and Market Sentiment

Beyond corporate fundamentals, consumer behavior is also shaping S&P 500 dynamics.

Rising oil prices—reportedly up significantly due to geopolitical conflict—have increased fuel costs, reducing disposable income and impacting discretionary spending.

This creates a feedback loop:

- Higher energy costs reduce consumer spending.

- Lower spending affects corporate revenues.

- Earnings pressure feeds back into stock valuations.

At the same time, market participants are finding opportunities in these conditions. Lower stock prices in certain sectors are being viewed as entry points for long-term investors, particularly in consumer discretionary companies.

Earnings Season: The Next Major Catalyst

One of the most critical near-term drivers for the S&P 500 is corporate earnings.

Current expectations suggest:

- Forward earnings growth: Approximately 17%

- Projected Q1 growth: Around 13%

Interestingly, the ratio of negative-to-positive earnings preannouncements is stronger than historical averages, indicating cautious optimism among companies.

What Earnings Will Reveal

The upcoming earnings season will test whether companies can:

- Maintain profitability despite rising input costs

- Pass higher costs onto consumers

- Sustain growth in a slower economic environment

Strong results could push the index back toward its previous highs, while disappointments may reinforce a bearish trend.

Technical Outlook: Key Levels and Market Signals

From a technical perspective, the S&P 500 is at a critical juncture.

Key Levels to Watch

- Resistance: 6,650–6,700

- Support: 6,500 and 6,313

A decisive move above 6,700 could signal renewed bullish momentum, while failure to hold current levels risks deeper correction.

Indicators Reflect Caution

- Relative Strength Index (RSI) remains below neutral

- Volatility (VIX) is elevated

- Market breadth remains weak

These indicators suggest that the market’s recent gains may not yet reflect a durable recovery.

The Bigger Picture: What the S&P 500 Represents Today

The S&P 500 is more than just a stock index—it is a reflection of broader economic forces:

- Technology transformation: AI and data infrastructure are reshaping industries

- Global interdependence: Geopolitical events directly influence market performance

- Policy sensitivity: Central bank decisions remain a dominant factor

In 2026, the index sits at the intersection of these forces, balancing optimism about innovation with concerns about inflation and economic stability.

Conclusion: A Market Defined by Tension—and Opportunity

The S&P 500 in 2026 is neither in clear recovery nor in definitive decline. Instead, it occupies a transitional phase marked by competing narratives:

- Strong earnings expectations versus rising cost pressures

- Sector outperformance versus weak overall breadth

- Technical stabilization versus macroeconomic uncertainty

For investors, this environment demands discipline and perspective. The index’s movements will likely continue to reflect a tug-of-war between resilience and risk.

What happens next will depend on a narrow set of variables: inflation trends, energy prices, corporate earnings, and central bank policy. Until clarity emerges, the S&P 500 will remain a market in tension—offering both caution and opportunity in equal measure.