Mortgage Interest Rates in 2026: A Market Under Pressure

A Market Defined by Volatility, Not Stability

Mortgage interest rates have entered 2026 in a state of tension—caught between economic uncertainty, geopolitical shocks, and shifting housing supply. For borrowers, lenders, and policymakers alike, the current environment is less about steady trends and more about rapid adjustments.

- A Market Defined by Volatility, Not Stability

- The Current Rate Landscape: Where Things Stand

- Why Mortgage Interest Rates Are Rising Again

- Affordability: The Real Impact on Buyers

- Housing Market Dynamics: Supply vs. Rates

- A Growing Concern: Mortgage Delinquencies

- Short-Term Trends: Volatility Remains

- Long-Term Outlook: Will Rates Fall?

- What This Means for Buyers and Homeowners

- Conclusion: A Market Redefined by Uncertainty

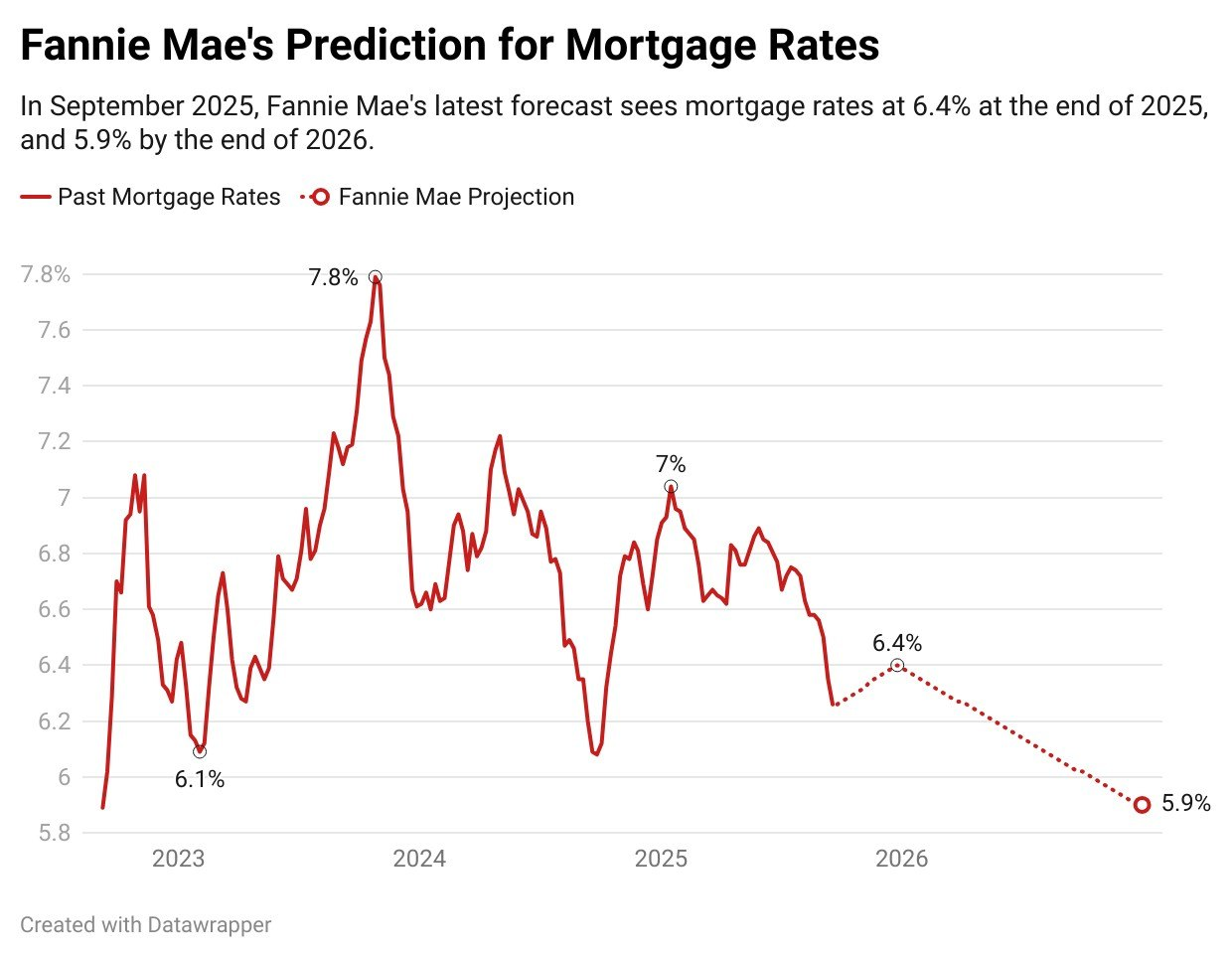

Recent data places the average 30-year fixed mortgage rate between roughly 6.45% and 6.50%, while 15-year loans sit closer to the mid-5% range. These figures represent a modest improvement from recent peaks, but they remain significantly higher than the historic lows seen earlier in the decade.

At the same time, even small fluctuations—such as a 40-basis-point increase—are proving enough to disrupt affordability and reshape borrower behavior.

The Current Rate Landscape: Where Things Stand

Key Mortgage Rate Benchmarks (April 2026)

- 30-year fixed: ~6.45%–6.50%

- 15-year fixed: ~5.57%–5.75%

- Jumbo loans: ~6.82%

These rates translate directly into borrowing costs. For example:

- A $100,000 loan at 6.45% costs about $629 per month in principal and interest

- Total interest over 30 years: ~$127,048

Even minor changes in rates can shift affordability thresholds for millions of buyers.

Why Mortgage Interest Rates Are Rising Again

1. Inflation Pressures from Global Events

One of the most significant drivers in 2026 has been geopolitical instability—particularly conflict affecting global oil supply chains. Rising energy prices increase inflation, and inflation pushes interest rates higher.

As explained through market dynamics:

- Higher oil prices → higher production and transport costs

- Higher costs → rising inflation

- Rising inflation → higher interest rates

This chain reaction has kept mortgage rates elevated despite earlier expectations of declines.

2. Bond Market Movements

Mortgage rates are closely tied to the 10-year U.S. Treasury yield. When bond yields rise:

- Mortgage rates typically rise as well

- Investors demand higher returns to offset inflation

Recent market turbulence has pushed bond yields upward, directly feeding into higher mortgage rates.

3. Federal Reserve Policy

The Federal Reserve does not directly set mortgage rates, but its policies strongly influence them.

- The Fed lowered rates in late 2025

- In 2026, it has paused further cuts, holding rates steady at 3.50%–3.75%

This pause signals uncertainty. If inflation persists, future rate cuts are not guaranteed—limiting downward pressure on mortgage rates.

Affordability: The Real Impact on Buyers

Mortgage rates do not exist in isolation—they directly affect what buyers can afford.

Monthly Cost Pressure

- Average monthly payment (principal + interest): $2,169

- Share of median household income: 28.9%

This is:

- Higher than February (27.7%)

- Lower than one year ago (30.8%)

Even so, affordability remains fragile.

Borrower Behavior

Cost sensitivity is now the dominant factor in decision-making:

- 75% of borrowers prioritize the lowest interest rate

- 54% focus on minimizing lender fees

However, behavior varies:

- Nearly 60% of baby boomers compare only one lender, indicating limited rate shopping

This gap suggests many borrowers may still be overpaying.

Housing Market Dynamics: Supply vs. Rates

Mortgage interest rates are interacting with a complex housing market.

Inventory Is Rising—but Unevenly

- National housing inventory: +8% year-over-year

- Still 11% below pre-pandemic averages

Regional differences are stark:

- Surplus markets: Florida, Texas

- Shortage markets: Northeast (up to 78% below normal levels)

Price Trends Reflect Supply Imbalance

- National home price growth: 0.4%

- Stronger growth: Northeast and Midwest

- Weakening prices: Western markets

Mortgage rates amplify these regional disparities—tight markets feel rate pressure more acutely.

A Growing Concern: Mortgage Delinquencies

Rising interest rates are not just affecting buyers—they are also impacting loan performance.

Key Findings

- 878,000 loans severely delinquent or in foreclosure

- 25% increase in four months

- Highest levels since 2018 (excluding pandemic spike)

FHA Loans Driving the Surge

- FHA loans account for 80% of the increase

- Cure rates dropped ~70% since late 2025

The expiration of forbearance programs has exposed underlying financial strain among borrowers.

Short-Term Trends: Volatility Remains

Despite recent small declines, mortgage rates are not stable.

- Rates fell about 0.20–0.25% in early April

- But had previously climbed above 6.6%

Market analysts emphasize that:

- Rates do not move in straight lines

- Short-term drops do not guarantee long-term improvement

There is still a credible risk of rates returning to high-6% or even low-7% levels if inflation intensifies.

Long-Term Outlook: Will Rates Fall?

What Could Push Rates Lower

- Declining inflation

- Economic slowdown or recession

- Federal Reserve rate cuts

What Could Keep Them Elevated

- Persistent inflation

- High energy prices

- Strong economic demand

Current projections suggest:

- Rates likely remain above 6% for the foreseeable future

- A return to sub-4% levels is unlikely

What This Means for Buyers and Homeowners

For Buyers

- Waiting for “perfect” rates may not be practical

- Rate fluctuations are unpredictable

- Delays may cost more in missed equity than saved in interest

For Homeowners

- Refinancing opportunities may be limited in the short term

- Financial preparation (credit, debt, savings) is critical

Strategic Reality

Mortgage interest rates are now a structural constraint, not a temporary anomaly.

Conclusion: A Market Redefined by Uncertainty

Mortgage interest rates in 2026 reflect a broader economic story—one shaped by inflation, global instability, and cautious monetary policy.

While rates have stabilized in the mid-6% range, the underlying conditions remain unstable. Borrowers face a market where:

- Small rate changes have large financial consequences

- Regional housing dynamics complicate affordability

- Loan performance risks are rising

The central takeaway is clear: mortgage rates are no longer just a number—they are a defining force in the housing economy, influencing everything from buying decisions to financial stability.